A Complete Guide to the Fraud Triangle, Fraud Diamond, and the Financial Systems That Protect Your Company

Employee fraud in a small business happens when an employee or trusted person improperly takes company funds or assets for personal use after being trusted with financial responsibilities.

Unlike external fraud, embezzlement typically involves someone inside the company who has legitimate access to financial accounts, payment systems, or company assets.

TL;DR: How Small Business Owners Can Detect and Prevent Embezzlement

Rather than have you click through to 6 different posts, this one is designed so you get it all in one read.

Embezzlement in small businesses doesn’t usually start with a career criminal, in fact, it’s quite the opposite. Most cases center around a trusted long-term employee who has huge financial pressure, access to company money, and believes they won’t get caught. Research in forensic accounting uses a couple graphics to show this. They’re called the Fraud Triangle (pressure, opportunity, and rationalization) and the Fraud Diamond, which added a fourth factor because computers entered the workplace: capability.

Small businesses are the most vulnerable because a small team means fewer internal controls, giving a single employee the opportunity to manage bookkeeping, payments, and the business’s financial records with little oversight.

The most common warning signs of embezzlement include employees who refuse to take vacations (which is mistaken as “a hard worker”), unexplained financial discrepancies, missing backup documentation, unusual vendor payments, and lifestyle changes that don’t match the paycheck they earn. Many fraud schemes go undetected for years unless owners actively monitor financial records.

Most embezzlement is discovered through employee tips, financial anomalies, internal reviews, or external audits. It’s surprising how often business owners ignore the gut feeling they had months before.

Small business owners can significantly reduce their risk by implementing a few core financial controls:

- Separate financial responsibilities so no one employee controls all transactions

- Require dual approval for payments and vendor changes

- Owners should open and read bank statements critically every month

- Review financial reports monthly

- Require independent reconciliation of accounts

- Require employees who handle finances to take actual vacations, not just extended weekends.

- Use accounting systems with audit trails and approval workflows

Done correctly, preventing fraud doesn’t reduce trust; the idea is to build systems that act as a deterrent, and make fraud difficult to commit and easy to detect. Businesses that implement basic financial controls dramatically reduce the chances of long-term embezzlement.

This guide explains why employee embezzlement happens (the Fraud Triangle and the Fraud Diamond), how to recognize the four warning signs, and the practical systems small businesses can implement to detect and prevent fraud before it becomes a serious financial loss.

What is embezzlement in a small business?

Embezzlement in a small business happens when an employee or trusted individual improperly takes company money or assets for personal gain after being trusted with financial responsibilities.

Unlike external fraud, embezzlement usually involves someone inside the company who already has legitimate access to financial accounts, payment systems, or company assets. That access is what makes embezzlement different from theft committed by an outsider.

Embezzlement happens when a person who is trusted with money or assets uses those resources for personal benefit without permission.The key element is trust. The employee committing the fraud already has legitimate access to company money and financial systems. This could be a bookkeeper, office manager, controller, or even a partner in the business.

In small businesses, embezzlement often involves actions such as:

- Writing unauthorized checks

- Creating fake vendor payments

- Creating fake employees

- Skimming cash from sales

- Altering financial records to hide missing money

- Reimbursing personal expenses through the business

At the Numbers Advisors we’ve seen sophisticated schemes that involved:

- Fake part-time employees with paychecks that increase slowly over years

- Vendor “shells” legally set up with FEIN’s and registered with the Secretary of State

- Credit cards in the business owner’s name, they didn’t know they had

- Approved paycheck advances that never get paid back

- Invoices from vendors marked as paid, but the vendor never got the check

Because the person handling these transactions may also be responsible for recording them, the fraud can stay hidden unless someone else reviews the financial activity.

Key statistics about small business fraud

Many small business owners think fraud only happens in big companies. In reality, small businesses are often more vulnerable because they have fewer financial controls and fewer employees to divide responsibilities.

The average embezzlement in the U.S. costs the typical business over $300,000.00 per episode, and fraud accounts for 30% of small business bankruptcies.

Research on occupational fraud consistently shows several patterns that every business owner should understand.

How common is embezzlement in small businesses?

Employee fraud is more common than many owners realize. “Asset misappropriation”, which includes embezzlement, is the most common form of occupational fraud in companies of all sizes.

Because of a lack of detection and reporting (for the various reasons that business owners may have), it is difficult to say exactly how common embezzlement is. It is estimated that 3-5% of businesses experience some form of “asset misappropriation.” The 3% number is more representative of the numbers that are positively discovered; the 5% number leaves room for the crimes that either aren’t discovered or publicized.

How long fraud typically goes undetected

Fraud schemes frequently continue for a long time before they’re uncovered. The ACFE reports that the median duration of workplace fraud schemes is approximately 12 months before discovery. Therefore, half of all embezzlement cases continue for more than a year before anyone notices something is wrong.

At the Numbers Advisors, we’ve had clients come to us after being victims of fraud that lasted almost 2 years and cost hundreds of thousands of dollars.

The longer a fraud scheme continues, the worse it gets because the employee becomes more comfortable with each check they write to themselves.

How most embezzlement schemes are discovered

Contrary to what many people think, most fraud isn’t discovered by audits. According to the ACFE, the most common way fraud is uncovered is through tips from employees (42% of the time), customers, or vendors who notice suspicious activity.

Tips are the most common way fraud is discovered. Tips only exist because there’s a second set of eyes looking at what’s happening in the business.

Financial anomalies also play a major role in detection. Unusual transactions, missing documentation, or inconsistencies in financial reports often reveal problems that need closer attention.

Why small businesses lose more to fraud than large companies

Large companies usually have stronger internal controls and separate employees who handle different financial tasks. It’s common for employees in large companies to have $1,000 limits on financial transactions with a secondary approval required by a ranking executive on anything larger.

Small businesses often rely on one trusted employee to manage multiple responsibilities like bookkeeping, paying vendors, and reconciling accounts. It’s common that those transactions are more than $1,000.

When financial duties are concentrated in one role with no oversight, it creates the opportunity that lets fraud happen. Small businesses often have:

- Fewer internal controls

- Less segregation of duties

- Limited financial oversight

- Smaller accounting teams

These structural factors increase vulnerability. The data confirms what many business owners already suspect. Without safeguards, fraud can cause serious damage. The question then becomes: How and when do you build these systems?

Understanding these patterns helps explain why strong financial systems and internal controls are so important. The next sections of this guide explain how fraud typically develops and what business owners can do to reduce their risk.

What embezzlement looks like in a small business

Many small business owners imagine embezzlement as a dramatic crime involving large sums of money and complex schemes. In reality, it often begins quietly and grows over time.

Most cases start with small transactions that go unnoticed. A trusted employee may reimburse a personal expense through the company or creates a small unauthorized payment. If the transaction isn’t discovered, the fraud continues and grows over time.

Because small businesses often operate on trust and lean staffing, these schemes can remain hidden for long periods. Understanding what embezzlement actually looks like in a small business is the first step toward preventing it.

How employee embezzlement usually begins

Most embezzlement schemes don’t start with a plan to steal large amounts of money. Instead, they often begin with a small decision that feels easy to justify.

An employee might have a personal financial problem such as debt, medical bills, or a family emergency. If they have access to company money and believe the transaction won’t be noticed, they may take a small amount with the intention of paying it back later.

If the transaction goes undetected, the fraud can escalate. What started as a small unauthorized payment can grow into repeated transfers, false reimbursements, or fabricated vendor invoices.

Over time, the employee may begin modifying financial reports to hide the activity. This is why many embezzlement schemes become more complex the longer they continue.

Why small businesses are especially vulnerable to internal fraud

Small businesses face a tough challenge when it comes to fraud prevention. Most companies simply don’t have enough staff to separate financial responsibilities across multiple roles.

In many businesses, one person handles several critical tasks at the same time, including:

- Recording transactions

- Paying vendors

- Reconciling bank accounts

- Preparing financial reports

When one person controls multiple parts of the financial process, it becomes easier to hide unauthorized activity.

Trust also plays a huge role in embezzlement. Small business owners often rely heavily on long-time employees who helped the company grow. That trust is important, but it can also reduce oversight.

Another challenge is limited time. Owners are usually focused on operations, sales, and managing their teams. As long as the business owner made payroll and paid their vendors, financial reviews fall to the bottom of the priority list, and that allows problems to develop quietly.

Some businesses reduce this risk by introducing independent financial oversight. For example, outsourced bookkeeping services or outsourced accounting can provide a second set of eyes on financial activity and help separate responsibilities that might otherwise fall to one employee.

Do most embezzlers get caught?

There is no exact percentage published for “how many embezzlers get caught.” That data is inherently difficult to measure because undetected fraud, by definition, is invisible.

However, the best available research gives us a clear and honest conclusion:

Not all embezzlers get caught, and many cases likely go undetected.

Here is what we do know from ACFE data and related research:

- Only detected and investigated cases make it into global fraud studies

- Because of business credibility, relationships with the fraudster, or the cost of prosecution, many companies decide not to report or pursue fraud cases publicly

- Researchers consistently acknowledge that actual fraud levels are higher than reported cases

Many embezzlers are eventually discovered, but it’s not accurate to assume that most are.

Do businesses get their money back?

This is where the data is much clearer, and more sobering.

According to ACFE research:

- 52% to 57% of businesses recover nothing after fraud occurs

- Only about 13% recover all of their losses

- The majority recover less than half of what was stolen

Even when the embezzler is identified, the money is often gone. It has usually been spent on an addiction or a lifestyle, hidden, or is simply unrecoverable.

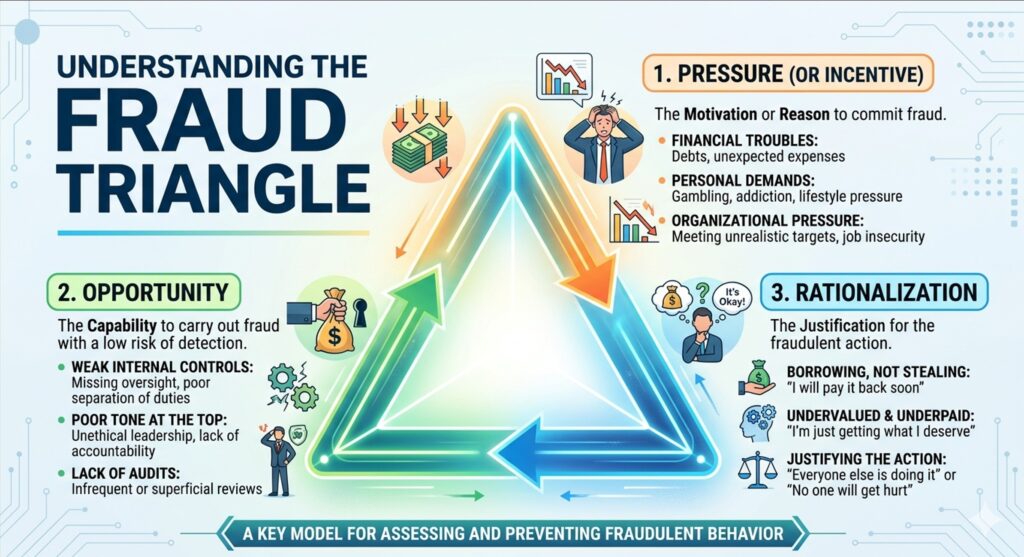

The Profile of an Embezzler: Understanding the Fraud Triangle

When small business owners think about fraud, they often picture someone who is dishonest from the start, maybe a fast-talking snake oil salesman, or a hacker grabbing a huge sum of money in one swipe. Embezzlement is different and usually the result of ideal conditions coming together, not just bad character.

One of the most respected models in fraud research is called the Fraud Triangle. It explains why trusted employees sometimes commit fraud. Understanding this model helps you recognize risk before it turns into loss.

The Fraud Triangle includes three elements: Pressure, Opportunity, and Rationalization. When all three come togeether at the same time, the risk of embezzlement increases.

The original text for this model is: Other People’s Money: A Study in the Social Psychology of Embezzlement (1953) written by Donald R. Cressey. Cressey’s work is one of the most quoted studies in the area of fraud.

What is the Fraud Triangle?

The Fraud Triangle was developed by criminologist Cressey after studying convicted embezzlers. He found most fraud cases shared the same three conditions.

These conditions are:

- Pressure

- Opportunity

- Rationalization

If one of these factors is missing, fraud is far less likely to happen. For small businesses, the most important factor is opportunity. This is the one piece you can directly influence through systems and oversight.

Pressure: The Hidden Problem

Pressure is the reason an otherwise good employee is motivated to steal. In many cases, the pressure is financial. Common motivating factors include:

- Personal debt

- Medical expenses

- Divorce costs

- Gambling problems

- Drug or alcohol addiction

- Lifestyle changes that outpace income

- Fear of losing a job

Pressure doesn’t automatically lead to fraud. Many employees face challenges and never commit a crime. In fact, 90% of people wouldn’t commit a crime even if they were guaranteed they wouldn’t be caught. But when pressure meets opportunity… the risk goes up.

As a business owner, you can’t always see an employee’s personal struggles. That’s why strong systems matter more than assumptions about character.

Opportunity: Weak Financial Controls

Opportunity exists when someone has access to company money and believes they won’t get caught.

In small businesses, opportunity is created when:

- One employee controls bookkeeping and payments

- Bank statements aren’t reviewed regularly by the business owner

- There’s no separation between recording transactions and approving them

- Financial reports aren’t reviewed in detail

- Vendor changes aren’t independently verified

- Payroll reports aren’t reviewed in detail

- Business owners don’t maintain relationships with key vendors

When financial responsibilities are concentrated in one role, your chances of suffering a fraud go up.

To further emphasize the growth of the opportunity side of the triangle, before 2003 the U.S. government didn’t worry very much about “leaking” and the opportunity for someone to become a spy was significantly smaller than it is today. But with the growth of electronic data and the internet, they now spend massive amounts of money to fight leaks. The ability to move money and information electronically has increased these threats exponentially.

This is where internal controls, independent reviews, and in some cases outsourced bookkeeping services can reduce risk. By introducing independent oversight, you reduce the opportunity component of the Fraud Triangle.

Rationalization: How Employees Justify Stealing

Most people who commit embezzlement don’t see themselves as criminals. Instead, they create explanations in their mind that make their behavior feel acceptable.

Common rationalizations include:

- “I’m just borrowing it.”

- “The company won’t miss it.”

- “I deserve this.”

- “I’ll pay it back later.”

- “They don’t pay me enough.”

- “I’m worth more than (employee name).”

This type of self-talk allows a person to maintain their self-image while still committing fraud. Notice how most of these defense mechanisms place blame on someone else. Fun fact: Interrogators reinforce these defense mechanisms when they’re getting a criminal to admit to a crime.

Small business owners often underestimate this part of fraud. Rationalization is powerful because it happens internally. Its not obvious. That’s why prevention should focus on reducing opportunity and strengthening oversight.

Why the Fraud Triangle Matters for Small Businesses

Small businesses are especially vulnerable because opportunity often happens more easily in lean teams. With fewer employees, it’s harder to divide financial responsibilities.

Understanding the Fraud Triangle helps change your focus from “Who would do this?” to “What conditions would let this happen?”

When you increase your awareness of pressure (talk to your employees about more than just work), limit opportunity with internal controls, and create clear financial systems, you significantly lower the risk of embezzlement.

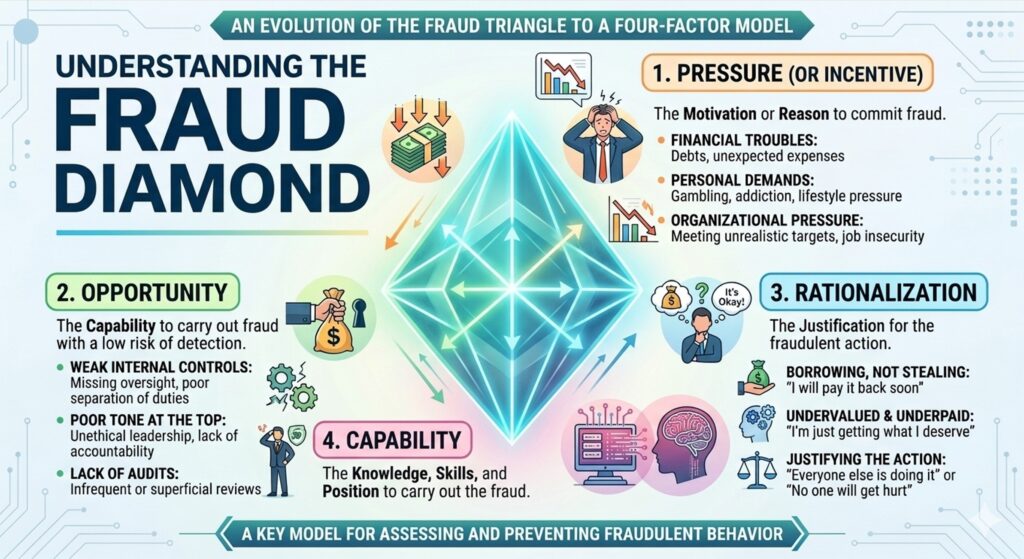

The next step in understanding fraud risk is learning the expanded model used by forensic accountants called the Fraud Diamond, which adds one more important factor…

The Fraud Diamond: Why some employees commit fraud

The Fraud Triangle helps explain why fraud happens. But forensic accounting research shows that understanding motive alone isn’t enough. Some people face pressure and opportunity, but still don’t commit fraud. Others do. The difference often comes down to capability.

That’s where the Fraud Diamond model becomes helpful for small business owners.

What is the Fraud Diamond?

The Fraud Diamond is an expansion of the Fraud Triangle. It was developed by forensic accounting researchers David Wolfe and Dana Hermanson. The Fraud Triangle includes pressure, opportunity, and rationalization, and the Fraud Diamond adds a fourth element called capability.

In simple terms, fraud usually requires more than just motivation. It also requires the know-how to carry it out successfully.

The four elements are:

- Pressure

- Opportunity

- Rationalization

- Capability

When all four components are present, the risk of fraud goes up significantly. For small businesses, this model is especially important because capability gets overlooked in prevention planning. The added irony is that the person you want to hire when you’re small can “do it all”; they have a broad range of skills and knowledge. Those same skills and abilities can be used to embezzle from you.

Capability: the missing element in fraud prevention

Capability refers to a person’s ability to execute and conceal fraud; you might say “sauvy”. This includes both skills and access.

An employee with capability likely:

- Understands accounting systems

- Knows how financial reports are generated

- Has access to bank accounts or payment platforms

- Knows how to adjust records without raising immediate suspicion

- Feels confident navigating internal controls

- May have some understanding of where an investigator would start looking

- Has a personality that’s either very persuasive or bully-like

Capability doesn’t necessarily mean they’re smarter than others. It means they have the right combination of access, knowledge, and control over financial processes.

In many small businesses, one trusted employee handles bookkeeping, vendor payments, and account reconciliations. That concentration of responsibility amplifies capability. It gives one person everything they need to both commit and hide fraud.

This is one reason why prevention strategies have to focus on system design, not employee trust.

Why capability matters in small business financial systems

Small businesses are built with small, lean teams. That structure is efficient, but it can unintentionally increase the risk of fraud.

When multiple financial tasks are assigned to one person, that individual may control:

- Recording transactions

- Writing checks or approving payments

- Managing vendor information

- Reconciling bank statements

- Preparing financial reports

If no one else reviews these processes, the employee has both opportunity and capability. Even strong internal policies may not be enough if the system allows one person to control the full financial cycle.

Business owners must design systems that limit both opportunity and capability. Without separation and oversight, even honest employees can eventually face conditions that increase your risk.

Capability matters because fraud is a process repeated several times over a long time; it’s not an isolated event. If someone understands how to manipulate records, adjust entries, or create false documentation, detection becomes more difficult. That’s why system design is more powerful than suspicion.

How business owners can reduce fraud capability

The good news is that business owners can significantly reduce capability through simple structural changes.

First, separate financial responsibilities whenever possible. No single person should control every step of a financial transaction. For example, the person who enters bills should not be the same person who approves payments.

Second, require an independent review of bank statements and reconciliations. Even in small teams, the owner can review financial reports monthly. This creates oversight without adding staff.

Third, use accounting systems that include audit trails and user permissions. Modern bookkeeping software allows owners to limit access based on role. This reduces the ability of one employee to alter records without detection.

Fourth, consider an outsourced bookkeeping firm or outsourced accounting services. When financial record-keeping is handled by an independent professional or firm, it naturally separates duties. This structure reduces both opportunity and capability. It also provides an additional layer of review that many small businesses can’t create internally.

Finally, build a culture where financial transparency is normal. When employees know that reports are reviewed regularly and processes are documented, the environment itself reduces th risk of fraud.

A common, affordable fraud prevention structure in a small business looks like this: Nobody inside the business opens the monthly bank statement except the business owner. The business owner critiques the bank and credit card statements every month. A valued person inside the company handles accounts payable and accounts receivable. Lastly, an outsourced bookkeeping service categorizes transactions and delivers monthly financials with remarks to the business owner.

The Fraud Diamond doesn’t suggest that employees aren’t trustworthy; it shows that fraud requires specific conditions. By reducing capability through system design and independent oversight, small businesses can significantly lower their exposure.

Understanding this model helps answer an important question many owners ask: why does fraud sometimes happen even in businesses that seem stable and well managed? The answer often lies in structure, not personality.

The next step in protecting a business is learning how embezzlement is detected and what signs to watch for.

How embezzlement is detected in small businesses

Many small business owners assume fraud will be obvious if it happens. The reality is that embezzlement starts quietly and grows over time. It starts with a “test transaction”, something small like an unauthorized payment or a minor adjustment in the books. If no one notices, the activity can continue for months or even years.

What are some examples of fraudulent “test transactions”

- The employee’s cell phone bill starts getting paid by the company

- Approved employee advances that don’t actually get paid back

- Extra items tucked into the company’s usual Amazon purchases

Research from the Association of Certified Fraud Examiners shows that most fraud schemes follow similar detection patterns. Once you understand those patterns, you know where to look.

The Most Common Ways Embezzlement Is Discovered

Embezzlement is rarely discovered by accident. In most cases, it’s uncovered through one of several common methods. The most frequent detection methods are employee tips, routine financial reviews, vendor concerns, and internal audits; in that order.

The ACFE’s global fraud research shows that fraud is often detected when another Someone notices an irregularity and raises a concern. That someone could be a coworker who sees unusual behavior, a vendor who questions a payment, or a business owner who reviews financial reports and notices something doesn’t look quite right.

Detection also happens when financial responsibilities change. For example, when a new employee takes over bookkeeping duties, they may notice inconsistencies in vendor records or bank reconciliations. Similarly, when an outside accountant reviews financial statements, discrepancies may be easier for them to spot.

The common thread in these situations is oversight. Fraud becomes much harder to conceal when multiple people are reviewing financial activity.

Why employee tips uncover the most fraud

One of the most surprising findings in fraud research is how frequently fraud is uncovered by employee tips. According to the ACFE’s Report to the Nations, employee tips are the single most common way small business fraud is detected.

This happens for one simple reason. Employees see things that financial reports don’t show. They notice unusual behavior, questionable transactions, or patterns that don’t make sense.

For example, a coworker might notice that an employee never allows anyone else to handle vendor payments. Another employee might see checks written to unfamiliar vendors. In some cases, staff members observe personal purchases being charged to the company card.

These small observations often lead to the first questions that uncover fraud.

This is why many organizations create confidential reporting systems or encourage open communication about financial concerns. When employees know they can safely report suspicious activity, fraud is more likely to be detected earlier.

Financial Discrepancies That Reveal Embezzlement

Financial records often provide the clearest evidence of embezzlement. Even well-hidden fraud usually leaves a trail in the accounting system.

One of the most common signs is a discrepancy between bank balances and accounting records. When bank statements don’t match the books, it signals that something may need further review.

Other discrepancies can appear in vendor payments, expense reimbursements, or unusual adjustments in financial reports. A pattern of missing receipts or unexplained journal entries may also indicate a deeper problem.

Small business owners sometimes discover fraud while reviewing their monthly profit and loss statement. If expenses suddenly increase without a clear explanation, or if cash flow doesn’t match sales activity, it can prompt a closer look at the underlying transactions.

The key point is that fraud almost always leaves a financial fingerprint. Regular financial reviews help uncover those patterns before losses get out of hand.

How Audits and Financial Reviews Detect Employee Fraud

Audits and financial reviews add another layer of protection against embezzlement. These processes are all about examining financial records to verify transactions are legitimate and correctly documented.

In big companies, internal audit teams perform this function. Small businesses usually rely on outsourced bookkeepers, outside accountants, tax professionals, or financial consultants to review records periodically.

During a financial review, professionals examine bank reconciliations, vendor payments, expense documentation, and accounting entries. Their goal is to confirm that financial transactions match the underlying business operations.

This outside perspective is valuable because external professionals often notice patterns that internal staff might miss. They don’t suffer the “can’t see the forest for the trees” problem. They’re trained to look for unusual transactions, inconsistencies in documents, and signs of manipulation in financial reports.

How Accounting Software and Audit Trails Expose Fraud

Modern accounting software has become one of the most effective tools for detecting employee fraud. Most accounting software now includes detailed audit trails that track who entered or modified financial information.

An audit trail records key information like the user who made the change, the date and time of the entry, and the original transaction details. If someone alters a payment record or deletes a transaction, the system keeps a history of that event.

This transparency makes it much harder to conceal fraudulent actions. Even if an employee attempts to modify the books, the system retains a record of the change.

Accounting software also allows businesses to control access to financial functions. Owners can restrict who’s allowed to create vendors, approve payments, or adjust financial records. These controls reduce the opportunity for manipulation.

For many small businesses, combining modern accounting software that’s set up correctly with independent outsourced bookkeeping oversight creates a strong defense against fraud. The system records the activity, and another set of eyes reviews the results.

Together, these practices make embezzlement far easier to detect before it causes serious financial damage. And when it’s known that these systems are in place, it serves as a deterrent.

Red Flags and Warning Signs of Embezzlement

One of the most common questions business owners ask is simple: What are the warning signs of embezzlement?

The challenge is that fraud rarely announces itself clearly. Instead, it shows up through small changes in behavior, financial activity, or day-to-day processes. On their own, these signals may seem harmless. Over time, they create a pattern.

Research and guidance from the Association of Certified Fraud Examiners and industry risk experts shows most embezzlement cases share a consistent set of red flags. The warning signs for fraud break down into four distinct areas: behavioral, financial, operational, and lifestyle changes.

Recognizing these changes is as important for any small business owner as is the skill of recognizing a driver drinking alcohol for the owner of a towing company. Learning to recognize these signs early can make a significant difference in your ability to spot employee fraud quickly.

Important note: Do not confuse the four warning signs of fraud with the 3 elements of the fraud triangle or the 4 elements of the fraud diamond.

Behavioral Warning Signs of Fraud

Behavioral changes are usually the first signs that something’s wrong. These changes can be subtle, and they’re easy to dismiss, especially when they involve a trusted employee.

One of the most commonly cited red flags is an employee who refuses to take time off. The reason this gets overlooked is because the business owner easily confuses this behavior for “hard work”. According to fraud research and industry guidance, employees executing an ongoing fraud scheme avoid vacations because they don’t want anyone else reviewing their work.

Other warning signs include increased defensiveness, reluctance to share financial information, or a need to maintain control over specific processes. You might hear things like “let me do it or it won’t be done right.” Again, the appeal to the business owners’ appreciation for quality work. An employee who becomes unusually protective of vendor relationships or payment systems may be trying to limit oversight.

The ACFE also points out that many fraud cases involve employees who appear reliable and trusted. This makes behavioral changes even more important to notice, because they might be the only early warning signal you get before financial discrepancies become obvious.

Financial Red Flags of Embezzlement

Financial records often reveal problems more clearly than behavior. Data don’t lie. Even well-concealed fraud creates inconsistencies in the numbers when examined closely.

Common financial red flags include unexplained expenses, missing documents (receipts, P.O.s, invoices), and irregular transaction patterns. You’ll see things like duplicate payments to vendors, frequent adjustments to accounting records, or transactions recorded outside the normal workday.

Industry sources such as Case IQ and other fraud prevention resources highlight that many embezzlement schemes involve small, repeated transactions rather than large, obvious theft. This makes them harder to detect without consistent review. Employee embezzlement happens at the edges.

Business owners may also notice that cash flow doesn’t match reported revenue, or expenses are going up without a clear business reason. These types of discrepancies often trigger an investigation.

Operational Red Flags in Financial Controls for Small Businesses

Sometimes the warning signs aren’t in the numbers, but they show in how the work gets done.

Operational red flags often point out weaknesses in internal controls. For example, if one employee is responsible for recording transactions, approving payments, and reconciling accounts, this system is built to add risk.

Other process-related concerns include allowing a lack of documentation, missing approval steps, or inconsistent procedures for handling vendor payments and expense reimbursements. You would expect to hear about it when documents are missing…

Fraud prevention guidance consistently emphasizes that weak processes create opportunity. When systems aren’t structured correctly, or well-built systems aren’t consistently followed, it becomes easy for unauthorized activity to go unnoticed.

Small business owners must insist on adherence to strong structure and process. They must place increased value on employees who take vacations and follow processes. Strong processes reduce both opportunity and capability pointed out in the Fraud Diamond.

Lifestyle Changes That May Signal Employee Fraud

Another set of warning signs comes from changes in an employee’s lifestyle. Embezzlers don’t save money; they spend it.

In some cases, employees who embezzle start spending beyond what their paycheck would reasonably support. This might include expensive purchases, frequent travel, or noticeable upgrades in living standards.

While lifestyle changes alone don’t prove fraud, they can raise questions when combined with other warning signs. The ACFE notes that financial pressure is a common driver of fraud, and in some cases, that pressure shifts into visible spending once money is misused.

It’s important to approach this carefully. The goal isn’t to assume wrongdoing, but to recognize patterns that might warrant a closer look at financial activity.

Why Many Warning Signs Are Overlooked

If everyone knows the warning signs, the obvious next question is: Why does everyone miss them?

In small businesses, the answer usually comes down to trust, time, and structure.

Owners trust long-term employees and don’t expect fraud to occur in their business. That trust can lead to less oversight, misreading the signals, and fewer questions about financial transactions and processes.

Time is a big factor. Many business owners are focused on operations, sales, and growth. Financial review doesn’t happen as often or as thoroughly as it should because they don’t have time, and they trust the person doing the work.

Lastly, structure plays a role. When financial responsibilities are concentrated in one role, there’s no second set of eyes to catch inconsistencies.

Fraud is rarely hidden perfectly. In most cases, the warning signs are there. The issue isn’t that the signs don’t exist. It’s that no one connects the dots early enough.

This is why strong financial systems, regular review, and outsourced bookkeeping services are so important. They turn seemingly disconnected warning signs into a clear pattern of signals that can be acted on before the problem grows.

Why Fraud Happens More Often in Small Businesses

Many business owners think fraud is something that happens in big companies. In reality, small businesses face a higher risk of embezzlement and employee fraud.

The reason isn’t that small business employees are less trustworthy; you’ve seen fraud at big companies make splashy headlines. It’s that small businesses operate with fewer people, fewer systems, and less separation of financial responsibilities. These structural challenges build in the conditions where fraud can take hold.

According to the ACFE, smaller companies tend to suffer higher losses relative to their size. 30% of business bankruptcies happen because of fraud. That makes prevention even more important.

Lack of Separation of Duties

One of the most common causes of fraud in small businesses is the lack of separation of duties.

In simple terms, the separation of duties means that no single person should control every part of a financial process. For example, the person who enters bills shouldn’t also approve payments and reconcile the bank account.

In many small businesses, one employee handles bookkeeping, writes checks, and reconciles accounts. This creates an environment where the same person can both commit and conceal fraud.

This is one of the biggest risk factors. When responsibilities are divided, it becomes much harder for unauthorized activity to go unnoticed.

Too Much Trust in Long-Term Employees

Trust is a necessary part of running a small business. Owners rely on their employees to keep the business running smoothly. Over time, that trust can grow into a sense that certain employees would never do anything wrong.

Workplace fraud research shows a very different pattern. Many fraud cases involve long-term, trusted employees who have built credibility in the business.

According to the Association of Certified Fraud Examiners, fraud is often committed by employees with established tenure (more than 10 years with the company) and access to accounting software. This doesn’t mean trust is misplaced. It means trust should be supported by systems.

When oversight is reduced because an employee is seen as trustworthy, the opportunity for fraud increases. That combination can create risk even in businesses with otherwise strong cultures.

Limited Financial Oversight by the Owner

For most small business owners, financial oversight becomes one more task on an already full to-do list. When financial review is inconsistent, problems can develop without being noticed. Successful fraud schemes rely on a lack of regular oversight.

The ACFE’s research shows that fraud frequently continues for months before detection because financial reports aren’t reviewed closely or regularly enough.

Even simple habits can make a difference. When owners review bank statements, profit and loss reports, and reconciliations each month, it becomes much harder for discrepancies to go unnoticed.

You don’t have to be a CPA to implement consistent oversight. It requires attention and a willingness to ask questions when something doesn’t look right.

Understaffed Accounting and Bookkeeping Roles

Most small businesses don’t have a full accounting department. Instead, they rely on a single bookkeeper, office manager, or administrative employee to handle financial tasks.

This approach is practical and cost-effective, but it creates risk that might not be worth the profit margin. When one person manages multiple financial responsibilities, there’s no natural separation of duties.

Understaffed financial functions increase exposure to employee fraud. Without independent review or shared responsibilities, errors and intentional misstatements are harder to detect.

This is one reason many small businesses turn to outsourced bookkeeping and advisory services or outsourced accounting services. By inserting an external professional into the process, owners can create a separation of duties at an economical price and add an extra layer of oversight without hiring additional full-time staff.

Small businesses aren’t inherently unsafe. But their structure often creates the conditions where fraud can occur if proper systems aren’t in place.

Understanding these risks is the first step. The next step is building practical systems that reduce those risks and protect the business over the long term.

How to Prevent Embezzlement in a Small Business

At some point, every business owner asks the same question: how can I prevent embezzlement in my business?

The answer isn’t a single policy or tool. Prevention comes from a set of habits and systems that work together; Internal controls. When they’re in place and used consistently, internal controls reduce the chance of fraud and make it easier to detect if something goes wrong. Even simple controls can dramatically reduce the risk of fraud.

The Importance of Internal Controls for Small Businesses

Internal controls are the policies and procedures that govern how money moves through your business. They define who can approve payments, who creates vendors in your accounting software, who records transactions, and how financial activity is reviewed.

In large companies, these systems are built into departments and roles. In a small business, they must be deliberate. Without them, even a trustworthy team can operate in a way that creates risk.

Embezzlement data shows that businesses with strong internal controls experience fewer fraud incidents and detect issues faster when they occur.

For a small business, this doesn’t need to be complicated. The goal is to create a structure around financial activity so that no single person has unchecked control.

Segregation of Duties: The Most Important Fraud Control

If there’s one principle that matters more than any other, it’s segregation of duties.

This means dividing financial responsibilities so different people handle different parts of a process. For example, one person enters bills, another approves payments, and someone else reviews the bank reconciliation.

The reason this works is simple. Fraud becomes much harder when more than one person is involved. It introduces accountability and creates natural checks within the system.

The typical small business has to use creative solutions to create this. Even partial separation, combined with owner oversight or outside review, can significantly reduce risk.

Dual Approval for Payments and Vendor Changes

One of the most practical ways to prevent employee fraud is to require dual approval for key financial actions.

This includes approving payments, adding new vendors, and changing vendor banking information. These are common entry points for embezzlement schemes, especially those involving unauthorized payments.

When two people must approve a transaction, it creates a natural pause in the process. That pause allows questions to be asked and details to be verified. It keeps honest thieves honest.

Many fraud cases involve a single individual creating and approving payments without oversight. Dual approval removes that opportunity.

For small businesses, this control can be implemented within accounting software or banking platforms, making it relatively easy to maintain.

Independent Bank Reconciliation

Bank reconciliation is one of the most effective ways to detect and prevent embezzlement.

This process involves comparing the company’s internal records to actual bank statements. It ensures that every transaction recorded in the books matches what occurred in the bank account.

The key is independence. The person who performs the reconciliation shouldn’t be the same person who handles payments or records transactions. Before the reconciliation is done, the business owner should open and review all of the transactions in the bank and credit card statements. After the reconciliation is done, the business owner should review the general ledger for reconciliation adjustments.

When reconciliations are done independently, discrepancies are more likely to be noticed and investigated. This simple step often reveals unauthorized transactions, duplicate payments, or missing money.

Regular Financial Review by the Business Owner

Everyone in the company should appreciate your authority to look at the financials in detail at any time, and they should never be offended by you exercising that authority.

Strong systems are no replacement for owner involvement.

Regular financial reviews do take time each month to look at key reports. This includes the profit and loss statement, balance sheet, accounts payable, accounts receivable, payroll reports, and bank statements. It’s not enough to look at one month. You should be looking at severals months side by side and looking at trends.

You’re not doing an audit; you’re staying familiar with the financial activity of your business. When owners review their numbers consistently, they’re more likely to notice changes that don’t make sense.

Research into fraud schemes shows that on average they last at least a year before being discovered. Regular review shortens that timeline and reduces the chances of fraud by increasing visibility.

This is one of the simplest and most effective habits a business owner can develop.

Mandatory Vacations and Job Rotation

Another effective and overlooked control is requiring employees to take time off and rotating responsibilities when possible.

A fews ago I had an HR Manager who worked for me. His father had been a banker back in the 50’s and 60’s. The bank required his father to take a two-week vacation every year. Not two weeks of vacation broken up over the year; a two-week vacation. While it was refreshing for the employee, it also gave the bank enough time to spot irregularities in his work if something fraudulent was being done.

Employee Fraud schemes depend on consistency. The person committing the fraud needs to maintain control over the process to keep it hidden.

When that employee is vacationing, even for a short period, someone else steps in. That transition can expose irregularities that would otherwise go unnoticed.

Industry guidance and fraud case studies frequently point to mandatory vacations as a simple way to uncover ongoing schemes.

Job rotation works in a similar way. When different people handle financial tasks over time, it becomes harder for any single individual to maintain control over a fraudulent process.

For small businesses, this may require planning, but even occasional role changes or temporary coverage can make a meaningful difference.

Financial Systems That Help Prevent Employee Fraud

Strong systems turn good intentions into real protection. Most small business fraud doesn’t happen because someone set out to build a bad system. It happens because there was no system at all, or because the system relied too heavily on one person.

When financial systems are clear, consistent, and reviewed regularly, they reduce both the opportunity and the ability to commit fraud. This is where many small businesses can make real improvements without adding a large internal team. Structure and visibility are key to preventing employee fraud.

Implementing Strong Accounting Controls

Accounting controls are the foundation of any fraud prevention system. They define how transactions are recorded, approved, and reviewed.

In a small business, strong accounting controls start with clarity. Every financial process should have a defined path. Bills are entered one way. Payments are approved a certain way. Reconciliations are completed on a set schedule.

When processes are consistent, it becomes easier to spot when something falls outside the norm. That’s often where fraud is first detected.

Strong controls also create accountability. When responsibilities are clearly defined, it’s easier to trace activity back to the source. This alone can discourage fraudulent behavior. When financial controls are violated, that is an employee disciplinary issue and should be addressed accordingly.

Even simple consistent controls can make a significant difference in reducing risk

Using Technology to Create Financial Transparency

Software based accounting systems provide a level of transparency that wasn’t available to small businesses before the 1990’s.

Most platforms today have features like user permissions, approval workflows, and audit trails. These tools let business owners control who accesses which financial data and what actions they can take.

Audit trails are especially important. They record who entered or changed a transaction, along with the date and time. This creates a clear history of financial activity.

When employees know their actions are visible and traceable, it reduces the likelihood of misuse. Sunlight is a great deterrent and a detection tool.

Technology also makes it easier for owners to stay involved. Financial reports can be reviewed in real time, and alerts can be set for unusual activity. This level of visibility helps catch problems earlier.

How Outsourced Bookkeeping Helps Prevent Embezzlement

By the numbers, $100K to $300K is a common amount for an embezzler to take out of a small business. You have a 1-in-50 chance of suffering this fate without proper systems in place. An outsourced bookkeeper costs the typical small business about $375/month. Over the course of an 18-month-long embezzlement that’s $6,750. If I told you that spending $6,750 could save you $200,000.00, and the $6,750 came with a professional liability and errors and omissions insurance policy, would you do it? If I told you that the $375/mo would make you more efficient and you could likely win the work to more to cover the fee because of the gained efficiency, would that help?

One of the biggest challenges in a small business is separating financial responsibilities. There usually isn’t enough people on the team to divide roles effectively.

Outsourced bookkeeping helps solve this problem.

When bookkeeping is handled by an external professional, it introduces a natural separation between the person recording transactions and the people handling day-to-day operations. This reduces the risk that one employee can control the entire financial process.

An outsourced bookkeeping service also brings consistency. Transactions are recorded regularly, reconciliations are completed on time, and financial reports are prepared in a structured way.

This consistency makes it easier to identify irregularities. It also makes sure that financial data isn’t being managed in isolation by a single internal employee.

How Outsourced Bookkeeping Services Improve Financial Oversight

(and how business owners mess it up)

Bookkeeping and Advisory services can provide a higher level of financial oversight and augment gaps in the structure of a small business.

This can include reviewing financial statements, analyzing trends, and identifying unusual activity. Because these professionals aren’t involved in day-to-day transactions, they can provide an independent perspective.

That independence matters. It allows for objective review without the bias that comes with internal roles or long-term relationships.

Outsourced bookkeeping also helps make sure financial processes are being followed consistently. If something falls outside the expected pattern, it’s more likely to be noticed and questioned.

For business owners who don’t have the time or background to review financials in detail, this level of support adds an important layer of protection.

So how does the small business owner mess this up?…

Simple. The abdocate (hand off) the relationship with the outsourced bookkeeper they hired to their office manager. Now, the very person they were trying to keep from having control of all accounting processes is back in control. If you’re going to do this, just fire the bookkeeping service and let your office manager embezzle from you.

Business owners must be the primary point of contact for their outsourced bookkeeper. Yes, your office manager or other right can talk and work with the bookkeeper, but the bookkeeper works for you and should communicate freely with you.

Why Independent Financial Review Reduces Fraud Risk

Independent review is one of the most effective ways to prevent and detect fraud.

When financial information is reviewed by someone outside the day-to-day activities of the business, it creates accountability. It also increases the likelihood that irregularities won’t happen and discrepancies will be identified early.

The ACFE’s research shows that fraud often continues because no one is looking closely enough at the numbers. Independent review changes that dynamic.

This doesn’t need to be complex. It can be as simple as having an outside professional review monthly financial statements or periodically examine key transactions.

The important part is that the review is consistent and independent. Over time, this creates a system where financial transactions are always subject to oversight. For small businesses, that structure can be the difference between catching a small issue early and dealing with a much larger problem later.

Fraud Prevention Systems for Small Teams

If you run a small business, you already know the challenge. You don’t have endless resources and a large accounting department. You may have one office manager, one bookkeeper, or a small administrative team handling everything.

That doesn’t mean you can’t build strong fraud prevention systems. It just means those systems need to be simple, clear, and consistently followed.

The goal isn’t complexity. The goal is to reduce opportunity, increase visibility, and make sure no single person has unchecked control over your financial activity. Even small teams can put effective systems in place when they focus on the right areas.

Financial Controls Every Small Business Should Implement

Every small business needs a core set of financial controls. These controls create structure around how money is handled and reviewed.

At a minimum, there should be clear rules for how transactions are recorded, how payments are approved, and how accounts are reconciled. These rules should be consistent and documented so everyone understands how the process works.

When controls are defined and followed, it becomes much easier to spot activity that doesn’t fit the pattern.

Process Controls for Approving Expenses and Payments

Approval processes are one of the most important parts of fraud prevention.

Every expense and payment should follow a clear approval path. This includes vendor invoices, employee reimbursements, and any changes to payment details.

Setting up a new vendor should require your review and approval. Unrelated vendors are a frequently used tool of embezzlers. When you review accounts payable, it’s not enough to approve the amount against an invoice. You should ask who the vendor is and why they’re a vendor.

When approvals are informal or inconsistent, it creates an opening for unauthorized transactions. A structured process minimized the chances that something gets through.

For example, requiring documentation for every expense and a second level of approval for larger payments creates a natural checkpoint. It gives someone the opportunity to ask a simple question. Does this make sense for the business?

Many fraud cases involve employee reimbursements or payments to vendors that were never properly reviewed. A consistent approval process makes fraud much harder.

Technology Systems That Reduce Fraud Risk

Technology can support your processes and make them easier to follow.

Modern accounting and payment systems allow you to set user permissions, require approvals, and track activity through audit logs. These features help make sure processes are followed consistently.

They also create transparency. When every action is recorded, it becomes much harder for someone to hide inappropriate activity.

Another advantage of technology is visibility. Business owners can review financial activity in real time, even if they’re not involved in the day to day process.

This combination of control and visibility is a powerful way to reduce fraud risk in a small business.

Creating a Culture of Accountability and Transparency

Systems and controls are important, but culture is the real magic.

In a small business, culture comes directly from the owner. When accountability and transparency are part of daily operations, employees are more likely to follow established processes and raise concerns when something doesn’t seem right.

This includes setting clear expectations around financial behavior, encouraging questions, and making it known that financial transactions are reviewed regularly. Employee tips are the most common way fraud is detected. That only happens when employees feel comfortable speaking up.

Creating that environment doesn’t require formal programs. It starts with open communication and consistent leadership.

When people understand that the business values transparency, accountability, and open communication, it becomes much harder for fraud to happen in your business.

What to Do If You Suspect Embezzlement in Your Business

Suspecting embezzlement is one of the most difficult situations a business owner can face. There’s often a mix of uncertainty, frustration, and concern about what to do next. You might even feel anger and self-doubt.

The way you respond in the early stages matters. Acting too quickly can create legal risk or allow evidence to be lost. Moving too slowly can allow the problem to continue.

Preserve Financial Records and Documentation

The first step is to preserve your financial records.

If embezzlement is happening, the accounting software, bank statements, emails, and supporting documents may contain critical evidence. It’s important to make sure those records aren’t altered, deleted, or overwritten.

This may involve securing access to accounting software, downloading bank records, and limiting changes to financial data until a review can take place.

In some cases, businesses also create backups of their systems at this point. The goal is to capture a clear snapshot of financial transactions before anything changes.

Preserving documentation early makes it much easier to find out what happened and to support any future legal or financial actions.

Avoid Confronting the Suspected Employee Immediately

It’s natural to want answers right away. It’s also natural to want to make it stop instantly. But confronting an employee too early can create problems.

If the employee is committing fraud, an immediate confrontation may lead to the destruction of evidence or attempts to cover up activity. According to the Fraud Diamond, this person likely has capabilities. It can also complicate any formal investigation.

Fraud professionals generally recommend gathering information first. This allows you to approach the situation with a clear understanding of the facts. Avoid the strong temptation to make it stop instantly until you’ve involved professionals.

There are also legal considerations. Accusing someone without sufficient evidence can expose the business to risk. Taking a little time to review records and consult professionals helps make sure that any action taken is appropriate and well supported.

Conducting an Internal Investigation

Once you’ve preserved the records, the next step is to start a structured review of financial activity.

An internal investigation typically starts with identifying unusual transactions or discrepancies. This may include reviewing bank reconciliations, vendor payments, expense reports, and journal entries.

The goal is to follow the trail of transactions and determine if there’s a pattern. In the vast majority of cases, small business fraud involves repeated transactions over time rather than a single incident.

Documentation is important throughout this process. Keeping a clear record of findings helps ensure that conclusions are based on evidence rather than assumptions.

For small businesses, this process can feel overwhelming. That’s why many owners bring in outside support to assist with the review.

When to Involve Legal Counsel or Forensic Accountants

There’s a point where outside expertise becomes necessary…

If the situation involves significant financial impact, unclear records, or potential legal action, it’s often appropriate to involve legal counsel or a forensic accountant.

Forensic accountants specialize in analyzing financial data to identify fraud and quantify losses. They can trace transactions, reconstruct records, and provide detailed findings.

Legal counsel helps ensure that the business handles the situation properly from a legal standpoint. This includes advising on employee actions, protecting the business from liability, and guiding next steps if recovery or prosecution is pursued.

An expert would recommend involving professionals when the situation goes beyond a simple internal review.

Frequently Asked Questions About Embezzlement

This section answers the most common questions small business owners ask about embezzlement, employee fraud, and prevention. These are based on real search behavior and supported by research from the Association of Certified Fraud Examiners and industry guidance.

How is embezzlement detected?

According to the ACFE’s Report to the Nations, the most common method of detecting fraud is through tips from employees or third parties. This happens because employees inside the business notice unusual behavior or transactions before issues appear clearly in financial reports.

Other common detection methods include reviewing bank reconciliations, identifying discrepancies in financial statements, and conducting audits. In many cases, fraud is uncovered when someone takes a closer look at activity that doesn’t seem to match normal business operations.

What are the warning signs of embezzlement?

Warning signs of embezzlement usually fall into four categories: behavioral, financial, operational, and lifestyle changes.

Behavioral signs can include an employee who avoids taking time off, becomes defensive about their work, or insists on controlling certain financial processes.

Financial red flags often involve unexplained expenses, missing documentation, or transactions that don’t align with normal business activity.

Operational warning signs include weak internal controls, lack of oversight, or one person handling multiple parts of the financial process without review.

Lifestyle changes show up when an employee starts living beyond their means or taking vacations that are more extravegant thany they used to take.

Industry resources and fraud research show that these warning signs often appear together. The key is recognizing the pattern early rather than dismissing each sign on its own.

Do most embezzlers get caught?

Many embezzlers are eventually caught, but not usually right away.

The ACFE reports that fraud schemes frequently continue for months before detection. This delay happens because fraud is hidden inside normal business activity and may not be reviewed closely.

Most cases are uncovered when a tip is reported by another employee, when financial discrepancies are reviewed, or when responsibilities change and a new person notices irregularities.

While detection does happen in many cases, the length of time it takes highlights the importance of strong internal controls and regular oversight.

How can a small business prevent embezzlement?

A small business can prevent embezzlement by implementing strong internal controls and maintaining consistent financial oversight.

The most effective steps include separating financial responsibilities, requiring approval for payments, performing independent bank reconciliations, and reviewing financial reports regularly.

Even simple systems can significantly reduce risk when they are applied consistently. The goal is to make sure that no single employee has complete control over financial activity.

Research from the ACFE shows that businesses with stronger controls detect fraud faster and experience lower losses.

How can businesses prevent employee fraud?

Preventing employee fraud involves both systems and culture.

On the systems side, businesses should implement clear approval processes, maintain accurate records, and make sure that financial activity is reviewed regularly.

On the cultural side, creating an environment of accountability and transparency encourages employees to follow processes and report concerns when something doesn’t seem right.

Combining structure with a strong culture creates a more effective defense against theft.

What systems reduce the risk of employee fraud?

The systems that reduce fraud risk are those that increase visibility and limit individual control.

This includes accounting software with audit trails, approval workflows for payments, and clear separation of duties. It also includes regular financial review by the owner or an independent professional.